Phones, computers, medical devices, and nearly all types of electrical devices have one thing in common aside from being an essential part of modern society: they all require a processor. Although they may not all need to be of the highest performance, those that do, are made in Taiwan, but more specifically made by Taiwan Semiconductor Manufacturing Company Limited. Taiwan Semiconductor Manufacturing Company Limited or TSMC is a Semiconductor contract manufacturing and design company headquartered in Hsinchu, Taiwan. Their operations consist of designing and creating microchips for companies such as Apple, Nvidia, and Huawei, along with nearly 500 more companies.

There are only three companies in the world that are able to manufacture super-advanced chips: Intel, Samsung and TSMC. Of the three companies, TSMC is the most significant. Firstly, South Korea’s Samsung has its own manufacturing business, however, it is small and is mainly used for its own products. Similarly, Silicon Valley-based Intel only uses their manufactured chips for their own products. Therefore, technology companies and chip designers that need state of the art manufacturing capabilities are left with only one option, TSMC. This lack of competition has enabled TSMC’s unique business model to flourish.

TSMC’s business model differs from any of its key competitors. Unlike Samsung or Intel, it is a “pure-play” foundry. This means that TSMC only operates on a contract basis and doesn’t offer any products of its own design, thus eliminating the risk of a product failing to sell. One of the main reasons there are so few other chip manufacturers is simply due to the fact it is extremely capital intensive, when making chips in the advanced 7, 5, 3 nanometer range. Therefore, with so little competition TSMC’s business model has seized enormous market share and enabled the creation of new chip designer companies that previously could not have existed due to the inability and incapacity to produce the chips they designed.

As a result of TSMC’s market dominance and effective management, it has experienced strong financial success. Since 2016, TSMC has grown its revenue by over 36% from 948 billion TWD ($33.6 billion) to 1.3 trillion TWD ($46 billion) Trailing Twelve Months (TTM). Moreover, the semiconductor manufacturer increased its net income from 2016 by 50% from 332 billion TWD($11.8 billion) to 500 billion TWD ( $17.8 billion) TTM, which indicates its ability to profit from expanding its current business operations. Spending on Research and Development for 2019 stood at 8.5% of total revenue or $2.96 billion, a major financial commitment and indicator that TSMC is investing in its growth and future potential. TSMC also offers a small dividend of 1.7%, however, it is by no means a dividend stock. Though the dividend payment is insignificant now, it is expected to increase gradually as the company matures. However, as it stands the payout ratio is currently 1.8% which shows there is still a lot of growth yet to be achieved and therefore the prospects of a significant increase in dividend is nowhere near.

TSMC has consistently demonstrated its commitment to remain the number one semiconductor manufacturer. Over the past three decades, TSMC has invested in 18 state-of-the-art chip making facilities in Taiwan alone, which serves as a testament that it is committed to be the leading chipmaker at the highest level for years to come. On the other hand, there is an argument that the concentration of the factories in Taiwan leaves TSMC vulnerable from natural disasters or unexpected geopolitical issues, especially with regard to its controversial relations with China. Although these concerns are just, they do not consider how successful TSMC has been managed and run as a business located in Taiwan which may not have been the case if they were located anywhere else. Take for instance, the coronavirus pandemic, which caused global havoc and affected factories in particular. Whilst in America and many other leading economies factories were shut due to many covid infections, Taiwan was able to minimise its cases to less than 1,000 people with only 7 covid related deaths, and therefore able to keep factories open. Furthermore, TSMC has shown its desire to diversify as this year it announced it would spend $12 billion to build a new fabrication facility by 2024 in Arizona. This is a sign that TSMC could begin to build more facilities in North America, which accounts for 65% of the company’s revenue, nevertheless, it is clear Taiwan will remain its main production location as it has been the most geographically convenient and well suited for the company since its founding.

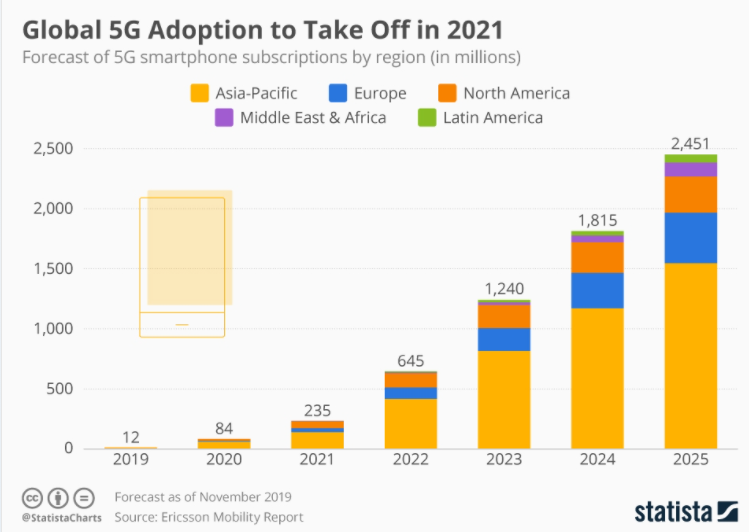

The introduction of 5G will generate even more growth and demand for TSMC. According to Statista, 5G is set to take off massively over the next 2-3 years and reach 2.45 billion people by 2025. In turn, this will cause a huge demand for 5G devices, in particular 5G mobile devices. This will stimulate huge orders for the most advanced 5 nanometer chips which only TSMC can make at such a capacity, compared to competitors like Shanghai’s Semiconductor Manufacturing International Corporation (SMIC), which is only able to manufacture 14 nanometer chips. A clear signal of this surge in demand can be seen by Apple, which has increased its iPhone production by 30% for 2021 with plans to produce nearly 100 million iPhones with 5G in the first half of 2021 alone. As a consequence, 5G will be the huge supporting factor for TSMC’s revenue growth and increase in demand for its 5 nanometer technology as many phone launches, in addition to Apple, will need the most advanced 5 nanometer chips and in large quantities which only TSMC can provide.

All the indicators point towards huge growth for TSMC, but a key question must be answered, how sustainable is this current rate of growth? To answer in the words popularized by legendary value investor, Warren Buffet, TSMC’s key ‘economic moat’ is that it is the founder and largest company of pure-play foundries holding a 50% + market share company to manufacture by contract. Therefore, this factor, along with the very high barriers of entry into the semiconductor business that limits new competitors, means that competition does not pose a major threat to revenue growth. However, though new competition may not cause financial damage, current high market cap clients such as Apple and Huawei could make all their own chips which would be a substantial loss considering Apple alone accounts for 1/5 of their revenue. Whilst this may be a damaging possibility, it is clear that current clients would only make chips for their own use and even so it would take years if not decades for them to replicate the same capacity that TSMC posses, consequently it is clear that TSMC will remain a massive provider and remain a significant part of the supply chain for at least the next decade or two. This is supported by Risto Puhakka, president of semiconductor analytics firm VLSI Research who said that “Wherever in the world it is, TSMC is a significant part of the supply chain,” and “There’s no avoiding it.”, showing that in one way or another these tech behemoths will still need TSMC services as it is the most advanced chipmaker, having built up experience and reputation in its specialised industry since the 1980s.

A final factor to consider is the environmental, social and governance side to TSMC’s business. It is critical to assess the ESG of TSMC’s business especially with ever increasing environmental regulations and a focus on a company’s ethics as it will show how TSMC will be shaped over the long term. TSMC have proven to be environmentally conscious having 910 gigawatt hours in the form of renewable energy and purchased carbon offsets. Additionally, the percentage of their waste sent to landfill has been below 1% for the past decade and waste materials recycled reached 96% in 2019, which is especially noteworthy for a business that is highly comprised of high power consumption factories. Moreover, with regards to its employees the average monthly salary of an employee in TSMC’s Taiwan facility was 3 times higher than the minimum wage in Taiwan. From this, one can see that TSMC has proven it is self aware and capable of taking into account these ESG factors whilst conducting its operations.

In summary, TSMC is an essential lifeline to some of the largest tech companies in the world and based on TSMC’s current performance and outlook this is unlikely to change. TSMC is in a highly unique position, from its experience and manufacturing capabilities, to benefit hugely from the introduction of 5G which will see a soaring demand for chips, of which TSMC stands to be by far the leading supplier.

RATE: $1 USD = 28.14 TWD