Howard Marks, co-founder and co-chairman of Oaktree Capital Management, recently spoke at Goldman Sachs stating that in order “to outperform you must hold a position different from the crowd”, adding that it will most likely make heads turn and cause controversy. With that said, there are currently few companies that spark as much controversy and turn as many heads as TSMC. Upon reflection of the geopolitical and macroeconomic events that have taken place since the last Sweeney Club article that was written on TSMC, in December of 2020, it is undeniable that prominent concerns over their impact on the chipmaker must be addressed. Some of the most significant events that have occurred include: the Russo-Ukrainian war, increasing geopolitical tensions between US/Taiwan and China, the shift in FED monetary policy and much more. Whilst there is ever growing uncertainty surrounding international conflict and fears over a global economic recession, it is important to take a step back and evaluate how significantly these changes have impacted TSMC, but crucially, how they affect the company’s future prospects.

How Safe Is TSMC?

is beyond dispute that the most worrisome question that haunts the minds of all TSMC investors is the possibility of an invasion of Taiwan by China. What we know for certain is that reunification is engraved in the PRC’s constitution as well as being supported by historical claims and laws such as the anti-secession law. On the other hand, the process of how this reunification could take place and whether it is successful or not is a different question altogether and this article does not intend to explore the countless possible scenarios involved and in no way intends to examine the politics behind the controversy, as it is impossible to predict accurately. However, it is nonetheless highly important to understand where TSMC currently stands in terms of global importance and why this safeguards its national security to a great extent.

Firstly, TSMC’s leading-edge fab facilities are all based in Taiwan, hence why the world relies on Taiwan for more than 90% of the most advanced chips on earth and why the company and country are linked so closely. TSMC has built a strong track record and reputation of reliably producing the most advanced chips, at the largest capacity, with the highest node yields and the most cost-efficiently which has caused it to become an essential part of the west’s technology infrastructure and to a larger degree an indispensable part of the digitalization of the global economy that was accelerated by the pandemic. Therefore, the extent of TSMC’s dominance has made it extremely difficult to replace both now and for the foreseeable future. Additionally, the global chip shortage has emphasised the importance of chips in the global economy, despite the shortage primarily relating to less advanced, relatively easier to manufacture chips used in products such as cars, thus demonstrating how detrimental a shortage of much harder to produce cutting edge chips (sub-5nm) would be. As a result, TSMC is of vital importance to the west, most notably the US and thus, the interest of Taiwan’s national security is, to a great extent, aligned with the US, especially when taking into account the US’ desire for influence in South-East Asia. Therefore, whilst TSMC’s crucial importance as the leader in advanced chip technology does not guarantee its safety, its current irreplaceability and highly destructive potential to hurt the global economy proves that the business itself will be prioritised to continue irrespective of the government in charge of Taiwan.

The Future

With the west finally awakening to its over reliance on Taiwan and thus TSMC, the question arises of who can replace the chip making giant and, crucially, how quickly. The governments of the US, Japan and South Korea alone have collectively committed over half a trillion dollars to domestic chip production by 2030. These expenditures will be aimed at improving domestic production primarily through funding R&D and building fabs with the ability to domestically produce chips ranging from the less advanced to the most cutting edge. However, despite the seemingly enormous amount of capital being deployed by governments over the next few years, it will do more good for TSMC than harm. This is primarily due to the fact that these projects will help subsidise TSMC’s new fab projects. In addition, the impact of the funding will primarily cause increased production of less advanced chips which will not harm TSMC’s profitability as more than 50% of TSMC’s total revenues come from highly lucrative cutting edge chips, with 20% of total revenues coming from 5nm chips alone. Moreover, even with these less advanced chips coming into higher supply, there is no certainty as to how cost effective they will be, what yields they will be able to produce and how powerful their performance will be relative to TSMC’s. Thus, TSMC’s long track record of consistently manufacturing the highest quality chips with its long lasting relationships, which stretch throughout the supply chain, will prove difficult to replicate even with large sums of capital and therefore does not pose a detrimental threat to TSMC’s business model and future market share.

Furthermore, it is commonly overlooked by policymakers and governments as to how difficult it is to not only become but remain a key player in the semiconductor manufacturing industry. This is primarily due to the capital intensive nature of the business and the challange of recruiting the most experienced talent with the right expertise and equipment to manufacture cutting edge chips. China is a prime example of how large sums of capital do not automatically guarantee the ability to make cutting edge chips. For instance, China has access to extensive natural resources needed for chip making such as silicon, of which it produced 6 million metric tons in 2021, more than double what the next 15 countries combined produced. Additionally, for the past decade China has committed hundreds of billions of dollars in R&D and capex as well as trying to buy ASML (a lithography machine crucial in making advanced chips) and using aggressive poaching methods to attract workers of TSMC. Despite its ongoing strong efforts, over the past decade it has not been able to achieve what the west now desires to achieve so quickly and what TSMC has proven to be the best at.

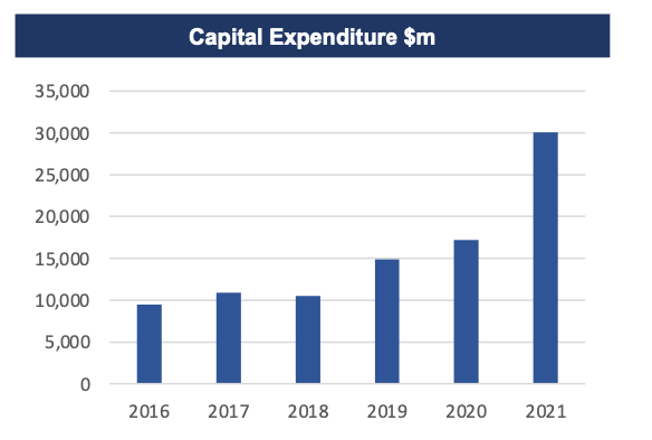

From this, it becomes more apparent that larger government spending and better recruitment of talent is required in order to replicate TSMC or even come close to competing, especially when taking a look at TSMC’s capex. Now retired TSMC founder, Morris Chang, called the amount of capital governments have committed to domestic chip production “too small” which at face value seems dramatic but becomes true considering TSMC’s commitment to spend $44 billion on capex this year alone, during rate hikes and other macro headwinds. This is not far off the largest economy’s commitment to spend $52 billion in the ‘CHIPS act’ that will be diluted down and allocated to a variety of different companies, including TSMC’s US fab facilities. The enormous capex which TSMC has a track record of spending since its founding is unmatched by any of its competitors and even though the size of capital deployed has demonstrated not to guarantee results, it seems much more feasible in the case of TSMC given their proven ability to effectively deploy such sizable amounts and how it has benefitted their business model over the past two decades. As a result, it is clear that it is highly unlikely governments will be able to catch up to TSMC in the course of the next few years and despite the geopolitical uncertainty TSMC is already benefiting from the wave of government subsidies as it diversifies manufacturing into Japan, US and further plans for more fab facilities. In turn, this will ultimately enable TSMC to continue its dominance as well as appeasing countries’ goals of increasing domestic production and not having to rely on a country at threat from invasion.

Strength Amidst The Paradigm shift

Finally, having established TSMC’s current importance due to the lack of an alternative and extremely low likelihood of its immediate replacement or significant reduction in market share despite the shaky geopolitical climate, it is important to consider how well it will fare given the fragile economy. It has become clear that microchips, referred to as the “new oil” by Intel CEO Pat Gelsinger, have become an essential commodity for the global economy and there are avenues for strong future growth that will shield the semiconductor industry and in turn TSMC from a recession to a large extent. For instance, in addition to the most microchip dependent sectors with the highest CAGR estimates for the next few years ranging from AI (39.18%) to EV (19.8%) to 5G networks (71.9%), military and healthcare spending are also set to experience huge growth with the semiconductor industry being a prime beneficiary of this spending. Whether it be an F50 fighter jet, a database centre for the CIA or an ultrasound machine for a hospital, microchips remain the most essential component. The healthcare sector is estimated to reach $6.8 trillion in the US alone by 2028 and due to the Russo-Ukrainian war, EU military spending is set to increase 123% for this year. As a result, the huge growth and investment into industries that all require chips will sustain demand and to a large degree reduce the negative consequences of a recession on TSMC.

Taking a look at TSMC’s financial strength, it becomes even more apparent how well it can fare during a recession and how rising interest rates will not have a detrimental impact. Firstly, TSMC has a strong and low leveraged balance sheet which can be seen from its low debt to equity ratio of 0.73 and long term debt burden totalling $23.3bn which proves insignificant relative to its cash on hand totalling over $46bn thus making the rise in interest rates less impactful due to the insignificant size of the debt relative to cash. Secondly, TSMC has seen significant increases in both its top and bottom line revenues. For instance, TSMC’s revenue grew 28% from $44.9bn in 2020 to $57.6 for TTM. Similarly, TSMC’s net income grew 44% from $15.2bn in 2020 to $21.9bn. As a result of the strong performance both during and in the aftermath of the global pandemic, TSMC has proven its ability to increase efficiency and profitability whilst at the same time expanding sales which in turn is a further testament of how capable TSMC’s management is in navigating through difficult macro environments. Therefore, the combination of a solid balance sheet, strong cash flows and effective management indicate that an economic downturn will not pose a serious threat to TSMC’s business fundamentals.

On the other hand, TSMC’s continued commitment to a high capex is an area of concern if the global economy is heading into a recession. TSMC has recently reiterated its plan to spend $44bn on capex in order to meet demand estimated to grow 20% over the next few years. However, a recession could significantly impact this estimate and cause a stronger consumer-end demand correction across smartphones to high performance computers that is already taking place, albeit not massively. Therefore, such high spending raises questions over how long it will take to reap the rewards of this record investment. Even though the slowdown in demand is already being felt by TSMC, their commitment to continued investment in their technology remains consistent with their successful business model and will give them an edge over the increasing number of government backed manufacturers. For instance, Intel has committed $27 billion towards its capex and it is expected to grow to $30 billion over the next 5 years. However, as demonstrated by failed competitors an increased capex does not guarantee success or technological breakthroughs especially as they do not have a strong record for successful capex spending and the large increase will require diligent allocation. TSMC on the other hand is dedicating up to 80% of their capex to work on advanced technology alone, thus highlighting its goal to lead in cutting edge chips technology. This record capex spending will also enable TSMC to remain ahead both in terms of the most advanced technology and in terms of cost-efficiency, thus whilst at face value seeming overly-ambitious heading into a recession, it will aid TSMC in remaining a leader in the industry, widening the gap between itself and potential competitors.

The Opportunity Now

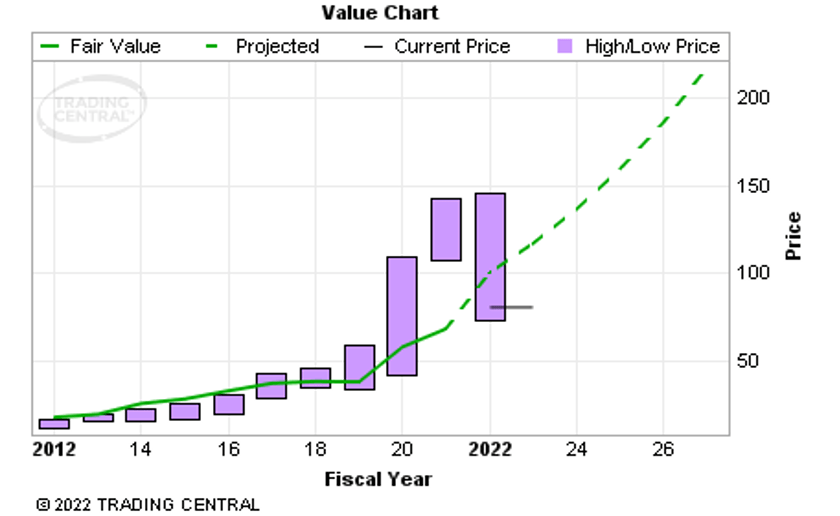

Due to the broader sell off and shift out of technology/growth stocks, over the past year semiconductor stocks have collectively posted negative returns, with TSMC down almost -35%. However, despite the weak performance and negative investor sentiment surrounding TSMC as well as many other semiconductor stocks, the current valuation has become even more attractive. TSMC’s American depository currently is trading on the NYSE: TSM at $80.90 per share (as of close on 02.09.22) with a PE ratio of 15.60, below both the industry average and the average of the S&P 500 index, representing discounted price 23.9% below the conservative fair value estimation of $100.29 per share.

Moreover, considering that in January at the start of this year $TSM was trading as high as $140 per share, prior to the Russo-Ukrainian war and heightened tensions between US/Taiwan and China, it is clear that the significant decline in price can be primarily attributed to the fearful sentiment of investors. This decline over since January further proves to be irrational considering the impressive fundamental performance beating expectations in Q1, with revenues up +35.5% and in Q2, revenues up +43.5%, net profit margin up +22.9% and net income up +76.8%. As a result, at the current price and overall valuation, TSMC offers the prospect of highly lucrative returns, however returns which investors must wait to reap the rewards of over the next few years.

All in all, a lot has changed externally in what surrounds TSMC, however, the business model itself remains fundamentally sound and on track to continue its long history of success with very few destructive impacts on the horizon. Therefore, it is pointless for investors to get caught up in the external noise of factors that do not prove to be fatal to the profitability and long-term future prospects of TSMC. Additionally, as proven, this is not a company that can suddenly disappear and be replaced overnight, especially not now with the western world having such a high level of dependence on its superior technology. Therefore, TSMC’s irreplaceability along with its current plans underway to diversify fab facilities out of Taiwan should give investors more peace of mind.

Finally, in the investment philosophy of Howard Marks, an investor with a reputation for consistent returns and outperforming during economic downturns, a ‘contrarian investor’ must be willing to stick to their investment thesis and hold an investment different from the crowd whilst being able to deal with the consequences that come along with it. It is beyond dispute that TSMC follows this philosophy and requires a ‘contrarian investor’ mentality to deal with the rollercoaster ride of media headlines and polarising views that hurt the short term stock price. Therefore, whilst not an investment for the faint-hearted, those brave enough to stick with TSMC through the controversy and short term declines have the potential to reap highly rewarding returns in the near future.