As advanced economies decarbonise over the next decade, a matter of crucial importance will be the supply of rare earth metals (elements 57-71, plus scandium and yttrium). These elements have important characteristics such as magnetism and heat resistance that make them vital for various areas of industry. Two elements of particular importance are neodymium and praseodymium. Together, they make NdPr, which is needed for NdPr magnets in the electric motors used in EVs. As EV sales skyrocket, demand for these NdPr magnets is expected to grow by 15X over the next decade. NdPr is also needed for the magnets found in wind turbines, drones, and robotics- all fast-growing areas.

What is particularly concerning in light of recent developments is that last year 85% of the global supply of processed rare earth metals came from China. Chinese restriction of rare earth metals supply has been touted as a possible weapon in the U.S-China trade war. In 2021, the Chinese Ministry of Industry and Information Technology asked rare earth metals miners about the potential impact of a supply restriction on U.S and European companies.The disastrous effects of Chinese supply restrictions were already seen in 2010, when, in response to the 2010 Senkaku boat collision incident, China cut off rare earth metals supply to Japan. Prices of neodymium outside of China went up 16X. Not only would China’s ability to restrict rare earth metals exports deprive the rest of the world of vital materials like NdPr for growing industries in the green economy, but such a move also gives advantages to Chinese firms who can benefit from comparatively lower input prices.

There do exist projects to provide NdPr that is sourced outside of China such as the Gakara project in Burundi and the expansion of facilities by Lynas, an Australian miner. After all, ‘rare earth metals’ is somewhat of a misnomer; rare earth metals are actually fairly common in the earth’s crust. The problem is that there are few known sites in the world with deposits that are sufficiently concentrated to be mined economically. This fact, coupled with the expected soaring demand, led Adamas Intelligence, an advisory firm that specialises on strategic metals and minerals, to predict an annual shortage of NdPr of 16,000 tonnes by 2030. This shortage, therefore, is expected to propel a significant uptick in NdPr prices over the coming decade.

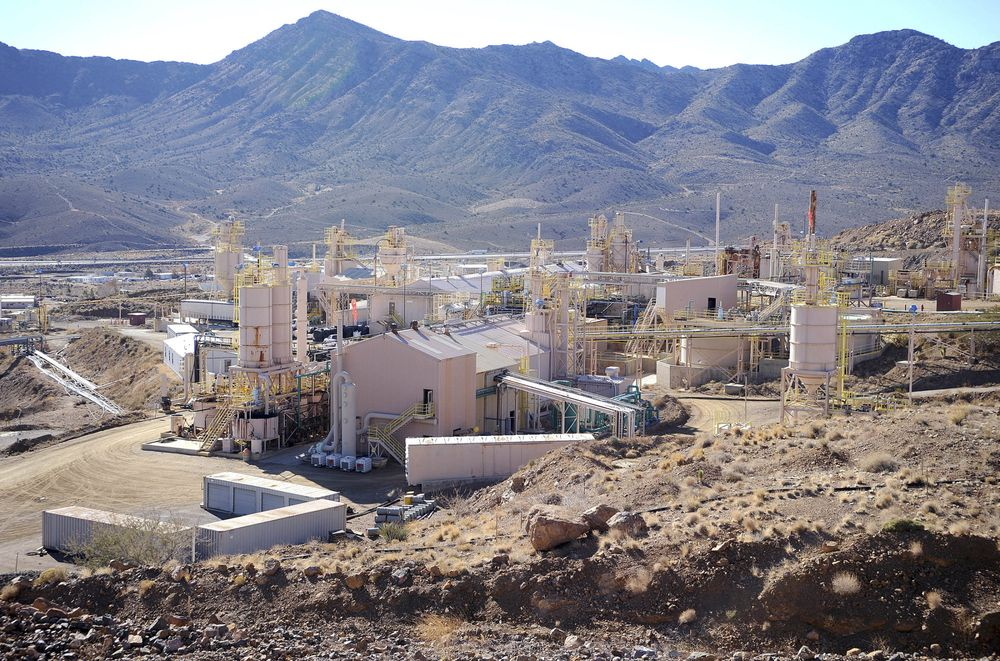

One fast-growing mining company seeking to profit from this development is MP Materials. It owns and operates Mountain Pass mine in California, the only rare earth metals mining and processing site in the entire Western Hemisphere. Having been founded in 2017, MP Materials already produces 15% of the world’s NdPr and, thanks to efficient production processes and its extremely high-quality ore it does so as the second lowest cost producer in the world. With plans underway to move beyond mining into refining their ore as well, MP Materials is setting itself up to be both a high-margin and strategically crucial company, the latter point being shown recognition through a $9.6 million grant by the U.S Department of Defense. MP Materials’s focus on NdPr, therefore, offers a pure play on the green economy revolution that the 2020s will continue to bring in.

What is especially attractive about the NdPr that MP Materials mines and plans to refine is that over 90% of electric vehicles require it for their motors and so the technology risk is low.

This is, for example, in stark contrast to metals that power certain battery technologies, of which there are many chemistries each requiring different metals. Forbidding some unexpected hitches in execution or an unforeseen dramatic upsurge in NdPr supply (both of which are unlikely), MP Materials is a company that seems poised to continue what has been so far some remarkable progress.